The Map That Became the Territory

How shareholder primacy undermined its own logic

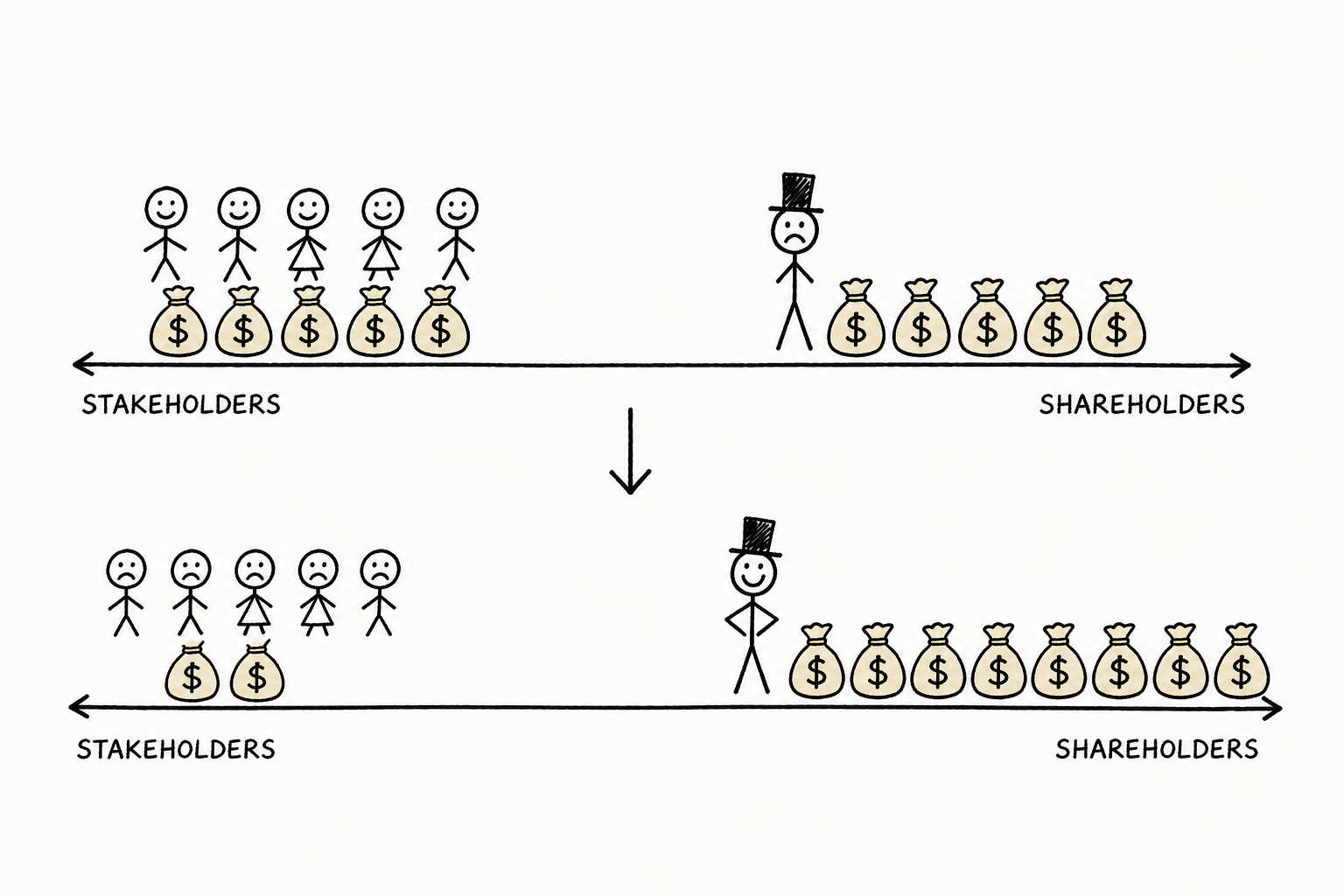

For four decades Costco paid above-market wages, held margins thin, capped the hot dog at $1.50, and built its model around member trust rather than member extraction.

In the early 2000s, these policies created friction with Wall Street analysts, starting with Bill Dreher at Deutsche Bank. Dreher said that “From the perspective of investors, Costco’s benefits are overly generous,” and “It’s better to be an employee or a customer than a shareholder”. If Costco would only treat its employees and members worse, there was so much shareholder value to be unlocked.

Costco’s founder Sinegal dismissed the pressure to cut employee benefits or raise prices for short-term gains. In a 2003 Fortune interview, he said: “We think when you take care of your customer and your employees, your shareholders are going to be rewarded in the long run. And I’m one of them [the shareholders]; I care about the stock price. But we’re not going to do something for the sake of one quarter that’s going to destroy the fabric of our company and what we stand for.”

There’s usually no way to adjudicate this kind of debate; the counterfactual doesn’t exist. In this case, it does.

Sam’s Club ran the Dreher playbook. It does less than half of Costco’s same-store sales and has half the profit per employee.

Wall Street analysts have updated their views on Costco. The doctrine they were applying has not. The specific case was absorbed as an exception. The doctrine that called Costco’s policies value leakage is more entrenched than ever. Buybacks are at record highs. Executive comp is more stock-price-tied than in 2005. Layoff-driven margin expansion is the standard playbook. Why didn’t the lesson take?

The usual explanations for why the lesson didn’t take, that analysts are short-sighted, that quarterly pressure distorts judgment, that finance culture rewards aggression, all point at behavior. The source of that behavior is structural. Measurement regimes are often treated as neutral, but neutrality and objectivity are different properties. An instrument can be perfectly objective about what it measures while being biased in what it has chosen to measure. The real power of any measurement regime lies not in the accuracy of its measurements but in the selection of what gets measured at all and in what, by exclusion, becomes invisible. The lesson didn’t take because the instruments the doctrine runs on can’t see the thing Costco was doing.

The Invisible Asset

What the instruments couldn’t see was trust capital: the value built through credibility, reliability, and consistency between a company and its stakeholders (employees, customers, and partners). Trust capital has three properties. Trust compounds by repeatedly making and meeting commitments, so it is built slowly. Like all other forms of trust, it can be destroyed much more quickly than it is built. Finally, it is structurally invisible to the measurement regime firms report against; accounting rules do not permit its recognition as it accrues.

This invisibility is the heart of the category error Wall Street analysts continue to make today. Wall Street analysts lean on quarterly earnings and discounted cash flow models to value firms. These instruments are built on accounting inputs, and accounting rules forbid recognizing trust capital as it accrues. No amount of tuning the model, longer forecast periods, different discount rates, or more generous terminal assumptions changes this. The asset is invisible to the inputs, so it’s invisible to the outputs. This is why analysts see the inputs to value creation as deductions from it.

The accounting profession isn’t completely blind to trust capital. When a firm is purchased for more than its book value, double-entry accounting requires the excess to land somewhere. That somewhere is goodwill. Aggregate goodwill on S&P 500 balance sheets is roughly $4 trillion, three times the cash those same firms hold. The accounting framework’s refusal to recognize trust capital during its accrual reflects a structural limit of the framework itself.

Goodwill can show up in a balance sheet only when a company is acquired, though it reflects an asset that was accruing the entire time. When brand reputation takes a hit, goodwill is marked down on the balance sheet. It can never be marked up. It’s an asset that defies the laws of physics; something that can be acquired, and destroyed, but never created.

The Ideology in the Machinery

This measurement regime is the machinery shareholder primacy runs on. When the doctrine says “maximize shareholder value,” what that means in practice is maximize what the instruments can see. Trust capital cannot appear in the inputs, so it cannot appear in the outputs. A firm building it looks like a firm wasting money. A firm depleting it looks like a firm unlocking value. The doctrine isn’t making a philosophical mistake about stakeholder primacy. It’s running on measurements that systematically misrepresent what firms are doing.

Shareholder primacy is the doctrine that a corporation’s purpose is to maximize returns for its shareholders. It licenses everything from aggressive buybacks to layoffs timed for earnings calls to the wholesale dismantling of research divisions that won’t pay back within the horizon an analyst model can see. It is treated, inside boardrooms and business schools alike, as the settled answer to the question of the purpose that firms exist to serve.

It has become a cultural norm, but it is not enshrined in American corporate law or case law. No statute requires directors to maximize shareholder value. The law gives directors and officers wide latitude, requiring only that they act in good faith, on an informed basis, and in the company’s best interests. Shareholder primacy is treated as a law of nature, but It’s an ideology, and like most ideologies its origin is traceable.

The modern version starts with Milton Friedman.

Before The Translation

When Friedman published “The Social Responsibility of Business Is to Increase Its Profits” in 1970, it landed amid a specific corporate pathology. ITT, under Harold Geneen, had grown from a telecom company into a $17 billion conglomerate (roughly $135 billion today) sprawling across Sheraton Hotels, Wonder Bread, Hartford Insurance, and dozens of other unrelated businesses.

Reporting requirements at the time aggregated results at the firm level, not the business unit, which meant outsiders couldn’t see which divisions generated value and which were being subsidized. The conglomerate form let managers cross-subsidize weak units with cash from strong ones, hide capital misallocation behind organizational complexity, and direct retained earnings toward empire-building rather than productive use. Friedman’s doctrine was a response to this. He saw managers operating with effectively no accountability to anyone, and argued that returning the firm’s purpose to a single, measurable objective would restore the discipline that scale had eroded.

His argument is structured around agency, not extraction. Managers, in Friedman’s framing, are agents of multiple principals: stockholders, customers, and employees. Taking from one to fund the manager’s personal priorities is, in his words, spending their money. The doctrine’s modern operationalization ( cutting wages to lift margins and raising prices to hit earnings targets) substitutes executive judgment for principals’ consent. By Friedman’s own standard, this is the violation his argument was meant to prevent.

Friedman explicitly endorsed trust capital. In the same essay, he described community investment as something that “may make it easier to attract desirable employees... reduce the wage bill or lessen losses from pilferage” and called the resulting goodwill “a by-product of expenditures that are entirely justified on [the firm’s] own self-interest.” He understood that relational investment produces returns. He saw no contradiction between his doctrine and a firm building trust capital.

The distortion came later. When the doctrine got operationalized through quarterly earnings and DCF models, the part of Friedman’s argument that depended on long-term relational investment became unmeasurable. What survived was the part the instruments could see.

Drawing Down The Account

Dreher’s criticism of Costco presupposed a fixed pool of money. The question in his mind was one of distribution; the generosity toward customers and employees could only come at shareholders’ expense. This is the firm as a redistribution problem. There’s a fixed pool of value and the question is how to divide it. Shareholders want more, stakeholders want more, and management strikes the balance. And because management’s primary compensation is stock, the balance tilts in one direction.

This frame is missing time. A fixed pool exists only in a given moment. Firms operate across years and decades, and the value they produce in year ten reflects the relationships they invested in during years one through nine. Costco’s brand is estimated to be worth $146 billion, about a third of its market cap. All of this value accrued after its founding. The redistribution frame can’t represent the process that produced it.

The firm is a nexus of long-term relationships, and the health of those relationships is shareholder value properly understood. This is the view Friedman articulated and Costco’s founders operationalized.

The analyst’s playbook is mathematically correct on its own terms. Cut wages, OpEx shrinks, earnings rise. Raise prices, revenue expands, earnings rise. What the math can’t see is that the savings are coming from somewhere: not from another P&L line, but from the trust capital the firm has spent decades building.

Trust capital depletion has the structure of drawing on a savings account that doesn’t appear on your statements. Decades of kept commitments, fair treatment, and restraint from extraction, all accruing to a balance the books don’t reflect. To people who only see the P&L, the withdrawals feel like found money because nothing on the books shows what’s leaving. The depletion only shows up later, in eroded customer loyalty, in higher employee turnover, through the slow unwinding of the relationships that were producing the returns in the first place.

Calling this zero-sum is too generous. The Sam’s Club playbook didn’t preserve the total, it shrank it. Same business model, different strategic choices, half the same-store sales and half the profit per employee. The strategies the analyst recommended weren’t redistributing the pie. They were shrinking it while transferring a larger share of the smaller pie to shareholders. This isn’t zero-sum capitalism. It’s negative-sum capitalism dressed in zero-sum logic.

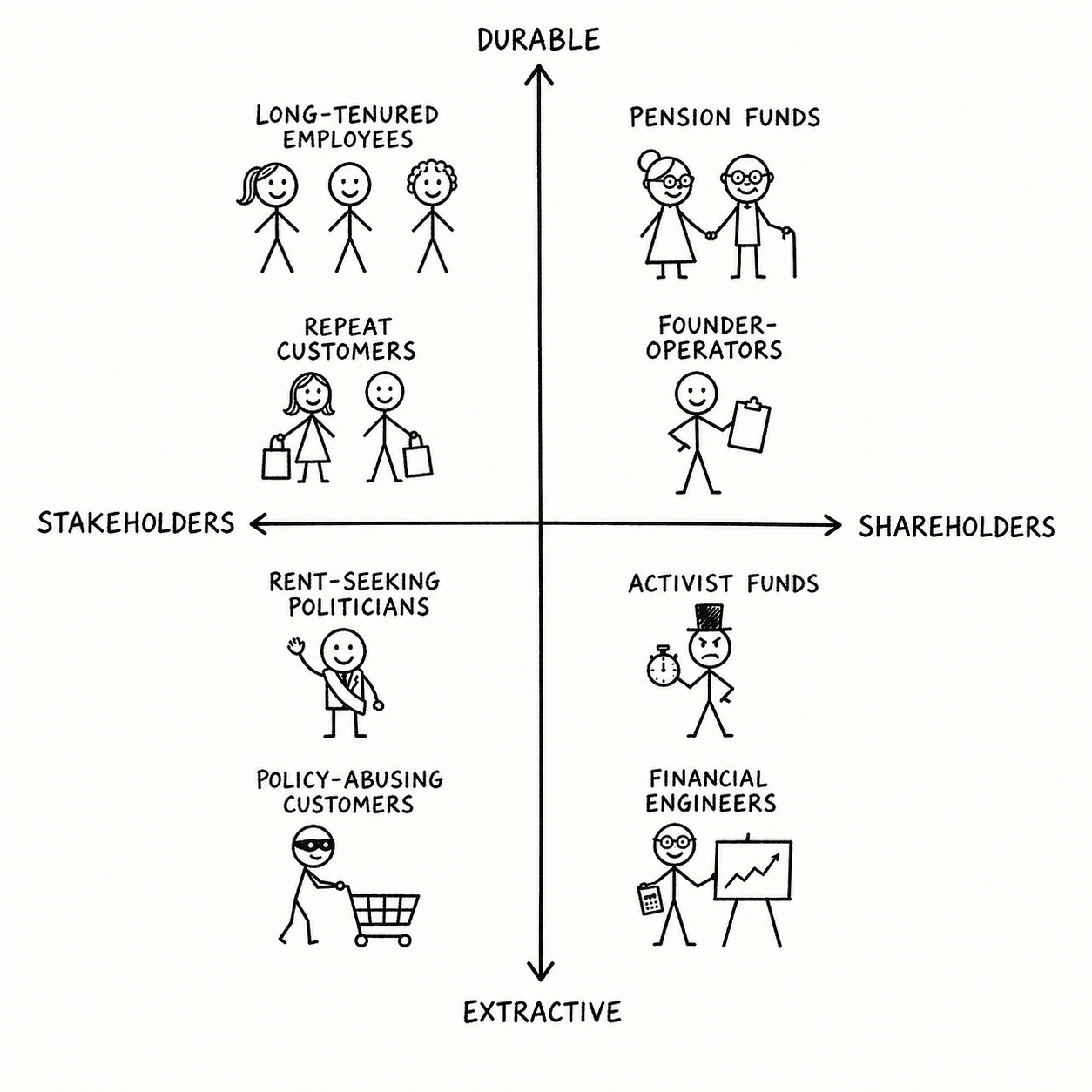

Competing Realities

The debate isn’t shareholders versus stakeholders. It’s durable capitalism versus extractive capitalism, and it exists on a different axis.

The durable quadrants form a coalition. Loyal customers, founder-operators, and pension funds all benefit when the firm continues to keep its commitments. Their interests compound together. The extractive constituencies are aligned in their intent, but are not a coalition. Extraction is a competition for finite spoils, and every group that drains value leaves less for the next extractor.

Once you see the coalitions, the original framing falls apart. The shareholder/stakeholder dichotomy assumed two coherent groups with opposed interests, with management in the middle balancing claims. The interests of durable shareholders and durable stakeholders run together. The opposition the framing insisted on was an artifact of looking at the firm at a single moment, with the time dimension stripped out. On any reasonable horizon, durable shareholders and durable stakeholders want the same thing: a firm that keeps its commitments and compounds the relationships that produce its value.

The Self-Fulfilling Doctrine

Friedman’s argument depended on things the system could not measure: multiple principals with competing claims, long-horizon investment, and the accumulation of trust.

When that argument was operationalized through quarterly earnings, discounted cash flow models, and stock-tied compensation, those elements did not survive translation. What could be measured became what counted, and what could not be measured was treated as if it did not exist.

What remained was the portion of the doctrine that fit the machinery: shareholder value maximization, expressed through quarterly earnings and stock price. The metrics began as compression, a way to make a complex objective legible to a system that needed numbers. Compression gave way to substitution as a signal of value creation became the target of optimization.

Over time, the map did not merely misrepresent the territory. It became the territory.

The substitution holds because the territory is not independent of the people operating on it. Firms run by operators who treat the firm as a redistribution problem become redistribution problems. Trust does not accrue because no one is investing in it. Durable coalitions cannot form because no one is offering the credible long-term commitments that would make them possible. The world becomes the world the map describes.

Sinegal believed the firm was something different and acted accordingly. Costco is the result.

Durable and extractive capitalism aren’t just competing views. They’re competing realities. The system will produce whichever reality its operators assume.